python algorithmic trading library

python algorithmic trading library

I would like to introduce some algorithmic trading libraries of python. I investigated the following four items this time.

zipline On github, it is the library with the most stars among the three. As a reference for how to use it, let's take a look at the code of algorithmic trading using DMA, which is also in the example.

import pytz

from datetime import datetime

import zipline as zp

start = datetime(1990, 1, 1, 0, 0, 0, 0, pytz.utc)

end = datetime(2002, 1, 1, 0, 0, 0, 0, pytz.utc)

data = zp.utils.factory.load_from_yahoo(stocks=['AAPL'], indexes={}, start=start,

end=end, adjusted=False)

class DualMovingAverage(zp.TradingAlgorithm):

def initialize(self, short_window=100, long_window=400):

self.add_transform(zp.transforms.MovingAverage, 'short_mavg', ['price'],

window_length=short_window)

self.add_transform(zp.transforms.MovingAverage, 'long_mavg', ['price'],

window_length=long_window)

self.invested = False

def handle_data(self, data):

short_mavg = data['AAPL'].short_mavg['price']

long_mavg = data['AAPL'].long_mavg['price']

buy = False

sell = False

if short_mavg > long_mavg and not self.invested:

self.order('AAPL', 100)

self.invested = True

buy = True

elif short_mavg < long_mavg and self.invested:

self.order('AAPL', -100)

self.invested = False

sell = True

self.record(short_mavg=short_mavg,

long_mavg=long_mavg,

buy=buy,

sell=sell)

import matplotlib.pyplot as plt

dma = DualMovingAverage()

perf = dma.run(data)

fig = plt.figure()

ax1 = fig.add_subplot(211, ylabel='Price in $')

data['AAPL'].plot(ax=ax1, color='r', lw=2.)

perf[['short_mavg', 'long_mavg']].plot(ax=ax1, lw=2.)

ax1.plot(perf.ix[perf.buy].index, perf.short_mavg[perf.buy],

'^', markersize=10, color='m')

ax1.plot(perf.ix[perf.sell].index, perf.short_mavg[perf.sell],

'v', markersize=10, color='k')

ax2 = fig.add_subplot(212, ylabel='Portfolio value in $')

perf.portfolio_value.plot(ax=ax2, lw=2.)

ax2.plot(perf.ix[perf.buy].index, perf.portfolio_value[perf.buy],

'^', markersize=10, color='m')

ax2.plot(perf.ix[perf.sell].index, perf.portfolio_value[perf.sell],

'v', markersize=10, color='k')

plt.legend(loc=0)

plt.gcf().set_size_inches(14, 10)

plt.show()

Looking at the code, the stock price history data is obtained using a function called

Looking at the code, the stock price history data is obtained using a function called zp.utils.factory.load_from_yahoo. This is of type pandas.DataFrame and has the same structure as the stock price data that can be obtained with pandas.

The main part of the algorithm is created by inheriting the zp.TradingAlgorithm class. By describing the processing to be performed for each time of the stock price in the handle_data function and assigning the value to the record function, it is possible to retrieve the data necessary for graphing the results. I am.

Regarding technical indicators, zipline itself has some indicator calculation functions, but by installing ta-lib, you can use more various indicators. Will be.

PyAlgoTrade The usage is similar to zipline, but it seems that it can handle live trade of Bitcoin and events of twitter. Let's take a look at the code of algorithmic trading using B Bands in samples as well.

from pyalgotrade import strategy

from pyalgotrade import plotter

from pyalgotrade.tools import yahoofinance

from pyalgotrade.technical import bollinger

from pyalgotrade.stratanalyzer import sharpe

class BBands(strategy.BacktestingStrategy):

def __init__(self, feed, instrument, bBandsPeriod):

strategy.BacktestingStrategy.__init__(self, feed)

self.__instrument = instrument

self.__bbands = bollinger.BollingerBands(feed[instrument].getCloseDataSeries(), bBandsPeriod, 2)

def getBollingerBands(self):

return self.__bbands

def onBars(self, bars):

lower = self.__bbands.getLowerBand()[-1]

upper = self.__bbands.getUpperBand()[-1]

if lower is None:

return

shares = self.getBroker().getShares(self.__instrument)

bar = bars[self.__instrument]

if shares == 0 and bar.getClose() < lower:

sharesToBuy = int(self.getBroker().getCash(False) / bar.getClose())

self.marketOrder(self.__instrument, sharesToBuy)

elif shares > 0 and bar.getClose() > upper:

self.marketOrder(self.__instrument, -1*shares)

def main(plot):

instrument = "yhoo"

bBandsPeriod = 40

# Download the bars.

feed = yahoofinance.build_feed([instrument], 2011, 2012, ".")

strat = BBands(feed, instrument, bBandsPeriod)

sharpeRatioAnalyzer = sharpe.SharpeRatio()

strat.attachAnalyzer(sharpeRatioAnalyzer)

if plot:

plt = plotter.StrategyPlotter(strat, True, True, True)

plt.getInstrumentSubplot(instrument).addDataSeries("upper", strat.getBollingerBands().getUpperBand())

plt.getInstrumentSubplot(instrument).addDataSeries("middle", strat.getBollingerBands().getMiddleBand())

plt.getInstrumentSubplot(instrument).addDataSeries("lower", strat.getBollingerBands().getLowerBand())

strat.run()

print "Sharpe ratio: %.2f" % sharpeRatioAnalyzer.getSharpeRatio(0.05)

if plot:

plt.plot()

if __name__ == "__main__":

main(True)

Like the

Like the zipline, it inherits the strategy.BacktestingStrategy class to create the main part of the trade. Compared to zipline, various data plot functions are prepared, and I feel that it is convenient.

pybacktest It is a lightweight library compared to the above two libraries. Let's take a look at the actual example code.

import pybacktest

import pandas as pd

ohlc = pybacktest.load_from_yahoo('SPY')

ohlc.tail()

short_ma = 50

long_ma = 200

ms = pd.rolling_mean(ohlc.C, short_ma)

ml = pd.rolling_mean(ohlc.C, long_ma)

buy = cover = (ms > ml) & (ms.shift() < ml.shift()) # ma cross up

sell = short = (ms < ml) & (ms.shift() > ml.shift()) # ma cross down

bt = pybacktest.Backtest(locals(), 'ma_cross')

import pylab

bt.plot_trades()

pd.rolling_mean(ohlc.C, short_ma).plot(c='green')

pd.rolling_mean(ohlc.C, long_ma).plot(c='blue')

pylab.legend(loc='upper left')

pylab.show()

You can see that the code is shorter than the two above. The class that actually backtests is

You can see that the code is shorter than the two above. The class that actually backtests is pybacktest.Backtest, but in the part before that, the time series data of the buy and sell signals is obtained in advance.

There are no functions such as calculation of technical indicators, and it feels like a library that simply summarizes the functions.

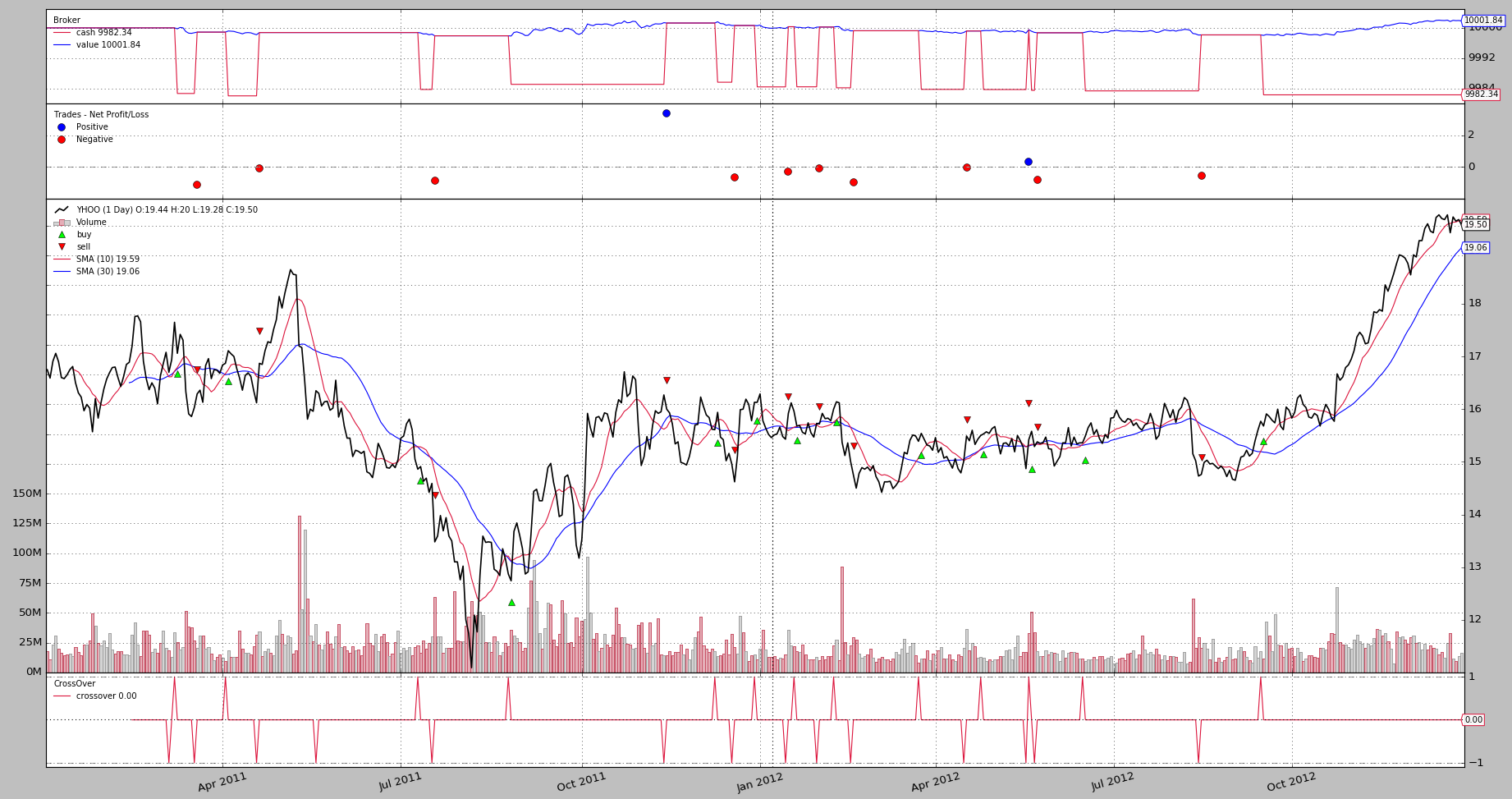

backtrader

from datetime import datetime

import backtrader as bt

class SmaCross(bt.SignalStrategy):

def __init__(self):

sma1, sma2 = bt.ind.SMA(period=10), bt.ind.SMA(period=30)

crossover = bt.ind.CrossOver(sma1, sma2)

self.signal_add(bt.SIGNAL_LONG, crossover)

cerebro = bt.Cerebro()

cerebro.addstrategy(SmaCross)

data0 = bt.feeds.YahooFinanceData(dataname='YHOO', fromdate=datetime(2011, 1, 1),

todate=datetime(2012, 12, 31))

cerebro.adddata(data0)

cerebro.run()

cerebro.plot()

Other

This is a python algorithmic trading library found elsewhere. ultra-finance QSTK

Recommended Posts